(Bloomberg Opinion) -- When third-quarter earnings reports come out in a few weeks, the bottom lines of companies in the S&P 500 are expected to be up an average of nearly 20 percent compared with the quarter a year earlier, signaling a continuation of good times for corporate America. Profits rose just more than 24 percent in the second quarter.

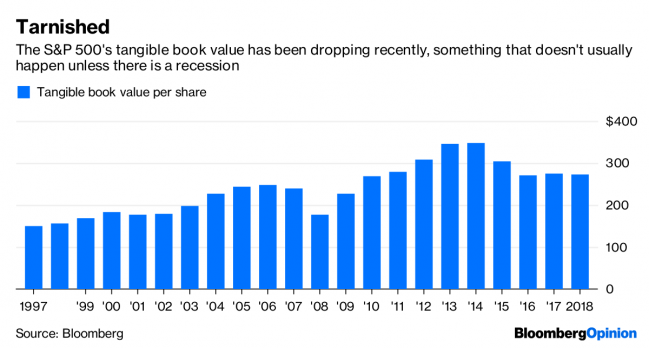

But another metric of financial health suggests all may not be as rosy as it first appears. The tangible net worth, or book value, of S&P 500 companies has been falling this year. The last time it had a sustained drop was right after the financial crisis in 2008. The time before that was in the previous recession in 2001.

The latest dip is not a new trend. The tangible book value of the S&P 500 companies peaked in 2014 and has dropped ever since. But tangible book values had begun to bounce back last year. What’s more, with this year’s dip, the S&P 500’s tangible book value has surrendered nearly all of its gains since the rebound from the financial crisis. At $2.45 trillion, the value, which is a calculation of assets minus liabilities, is the lowest since the end of 2010.

Several trends are converging to deflate corporate net worths. Low interest rates have encouraged borrowing, doubling corporations’ debt load in the past decade, which subtracts from book value. Stock buybacks, too, thanks to the change in the tax law, have boomed this year. That drains cash from corporate balance sheets and has also lowered book values. But the fact that earnings are not adding enough new cash to refill corporate capital buckets and then some is also contributing to the drop. Despite the jump in earnings, cash flow from operations is up much less, just 4 percent in the past 12 months, compared with the period a year earlier.

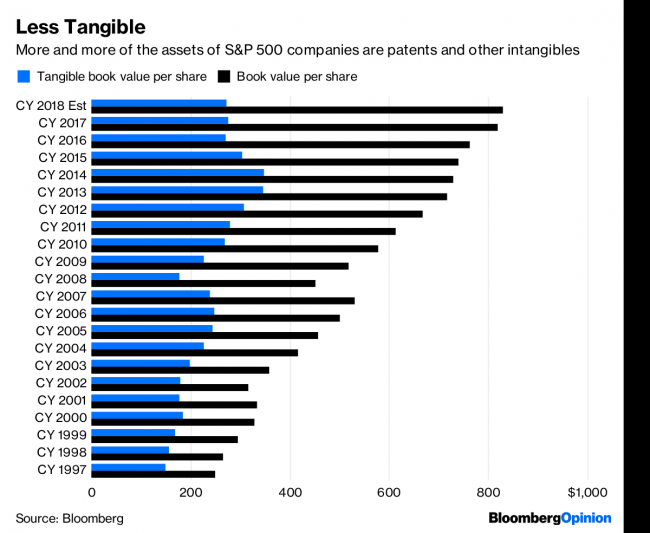

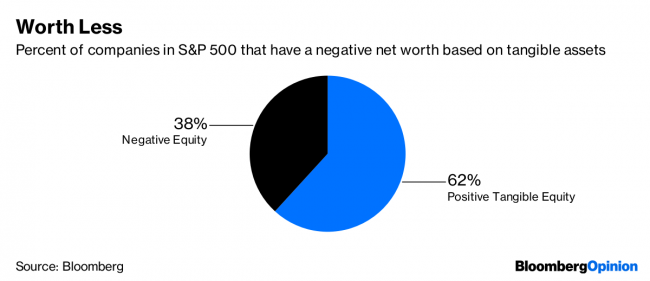

The result is a good portion of the companies in the S&P 500 effectively have a negative net worth. And that portion is growing. There are now 191 companies in the S&P 500 that have net tangible book values below zero, up from 124 five years ago. The furthest into the red is AT&T Inc (NYSE:T)., which has a tangible book value of a negative $129 billion. It is followed by fellow telecom and rival cable companies Verizon Communications Inc (NYSE:VZ). and Charter Communications Inc. General Electric (NYSE:GE) Co. is fourth, with negative tangible net worth of $47 billion. Some argue that because so many companies’ tangible book values have gone into the red — and are able to stay there with little repercussions — that the metric is no longer useful. Shares of Charter Communications (NASDAQ:CHTR), for instance, are up 123 percent over the past five years. The switch to an economy driven less by manufacturing and more by service and technology industries, in which patents and brands matter more than plants, may be a big driver in the drop in tangible book values. The S&P 500’s total book value, which includes the value of patents and other so-called intangible assets, has continued to increase.Nonetheless, the erosion of the tangible part of book value, which accounts for about a third of the total now, down from half five years ago, is not just about technology. Of the roughly $1.7 trillion growth in the gap between total book value and tangible book value, only about $70 billion comes from the growth in intangible assets, like patents, in the S&P 500’s information tech sector. Instead, a big driver of the growth in the tangible book gap is acquisitions and consolidation. About $750 billion of the gap is due to the growth in goodwill, which now totals just less than $3 trillion for the S&P 500. That’s the amount companies pay for acquisitions above book value. That could represent brand or some other value, but it could also just indicate that the acquirers overpaid. Presume it’s the latter and the stock market may be even more overvalued than it looks. The S&P 500 now trades at 3.5 times total book value, compared with an average of 3 times going back two decades. On the other hand, based on its tangible book value, the S&P 500 is trading at 10.6 times, compared with a 20-year average of just 6.4 times. The bull market is being driven more by air than the growth in real assets. If you think that air is the new lifeblood of the economy, then this may turn out just fine. If not, the market could be gasping soon.